With the financial year just ending, your next big task would be to calculate any tax on income other than your salary.

If you are sitting down to calculate your gains on debt funds that you had held for more than a year and sold in the just ended financial year, do consider the capital gains index or cost inflation index .

Long-term capital gains

Long-term capital gains (held over a year) on debt funds suffer a 10% tax without indexation or 20% with indexation benefit. In the case of the latter, by indexing, you bring your cost of investment to the current value, after factoring general price rise for consumers.

Given that the capital gains index has been expanding at a good pace (see table below), courtesy inflation, using the index will likely ensure that you pay very little tax or nil tax on your gains.

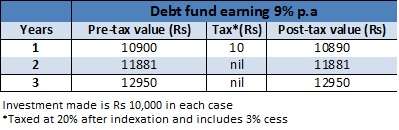

Let us take an example of a debt fund, say an income fund, that you bought for Rs 10,000 in 2011-12. If the fund returned 9% and you sell it for Rs 10,900, your long-term capital gain would normally be Rs 900. A 10% tax on this plus cess would be Rs 93.

But if you index the cost of the same with the CII for 2010-11 and 2011-12 and 2012-13, then the cost would be Rs 10,853.5 (10,000*852/785). So your gain, for tax purposes, would be Rs 46.5 (10,900-10,853.5). A 20% tax on Rs 46.5 will be just Rs 9.3.

With the same return, you may not even have to pay tax if you held the fund for say 2 years or 3 years, as the post-indexation cost will be higher than your sale value. For instance, assuming your returns were the same 9% annually, if you index your cost for 2 years, it would be Rs 11,983, as against sale value of Rs 11,881, resulting in a capital loss for tax purposes.

Hence, make a quick calculation of your gains post indexation before you pay your tax in the next few months.

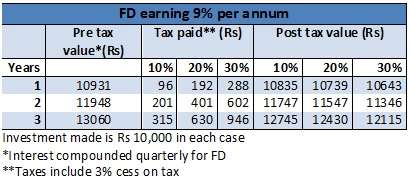

Comparison with FD

See the tables below to know how indexation makes a debt fund a superior post-tax product compared with FD, assuming that they earn the same returns.

It is noteworthy that even if you are in the 10% tax bracket, your post-tax returns would be lower in a fixed deposit. The difference widens if you are in the 30% tax bracket. If you are not a tax payer, only then, you may benefit from holding FDs (depending on whether FD returns are superior or not to debt funds).

Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan

2.Reliance Tax Saver (ELSS) Fund

3.HDFC TaxSaver

4.DSP BlackRock Tax Saver Fund

5.Religare Tax Plan

6.Franklin India TaxShield

7.Canara Robeco Equity Tax Saver

8.IDFC Tax Advantage (ELSS) Fund

9.Axis Tax Saver Fund

10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online -

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

---------------------------------------------

Invest Mutual Funds Online

Download Mutual Fund Application Forms from all AMCs

0 comments:

Post a Comment