Are you enamoured by the attractive offers, especially the gold savings plans offered by jewelers this Akshaya Tritiya? 'Pay 11 instalments and get the 12th instalment free', 'no wastage charges', 'enjoy loyalty club benefits' and so on are some of the 'offers' that these schemes lure you with.

Let us take one such scheme offered by a popular jeweler in the country: you pay 11 instalments for the gold scheme and the jeweler contributes towards the 12th instalment. That means if you save Rs 3,000 a month in a gold scheme with a jeweler for 11 months – paying Rs 33,000 over the tenure, you get to buy gold worth Rs 36,000 at the end of the tenure. If you think that's a big deal, then read on.

No Averaging

In schemes such as the one above, you are not allotted gold for every instalment that you make with the jeweler. That means the gold you are eligible to buy would be at the prevailing market price at the end of the term.

Let us suppose gold is Rs 2,895 a gram when you pay your first instalment. At the end of your 11th instalment, its price goes up to Rs 3000. That means you get to buy the jewellery at Rs 3,000 a gram and not at lower rates that may have prevailed earlier. In other words, you have no option to average your price of gold, although you pay an instalment every month.

It also follows that the Rs 3000 that the jeweler is contributing as the 12th instalment may actually fetch you a lesser gold equivalent. For instance, Rs 3000 paid by the jeweler would bring you just 1 gram, instead of 1.03 grams (at the beginning of the period in our illustration). Of course, you can argue that prices may come down. But then, would you be able to time your instalments knowing that prices are coming down?

You are Lending Money

On the face of it, you might seem to get a discount of 8.3% (Rs 3000 on Rs 36,000) in the above illustration. But is that really the case? By paying 11 instalments without any allotment of gold, you are effectively lending money to the jeweler. If a jeweler were to borrow outside, it would be anywhere between 10-18% for a loan, depending on the credit worthiness of the company. Hence, your money is a 'low-cost' credit line for him.

High Default Risk

Even assuming that the Rs 3000 you get is a form of interest for the money you lend for the tenure of the scheme, is your money in safe hands? Well, none of the jewelers' schemes guarantee you gold and there is no separate body/trust safeguarding your money. And to add to it, since you do not have any units allotted (in the above illustration), there is always a possibility that you do not get gold if your jeweler decides to bid you goodbye.

In fact recently, a change in the deposit-taking rules under the Companies Law has large jewellery makers in a fix as the money that they take from you on the schemes may come under the Company Law radar, in which case, many of them may withdraw their schemes. You can click here to read more on this news.

Not a Pure Deal

As you may be aware, jewellery schemes allow you to buy only jewels which are of lower purity, often 22 karat or lower. This reduces the resale value of such gold as well.

Besides, you seldom get to buy jewellery for the value you have saved. In the above example, you may have Rs 36,000 at the end of the tenure but you may wish to buy jewels that are valued at Rs 50,000. Effectively, you not only offer a cheap loan to the jeweler but also enhance his business!

No Wastage…Really?

Do read the fine print or the '*' that comes in the advertisements when it says no wastage. This is seldom the case. Often times, the wastage on designer jewellery is quite high that even if there is a small waiver on wastage, you seldom stand to gain much.

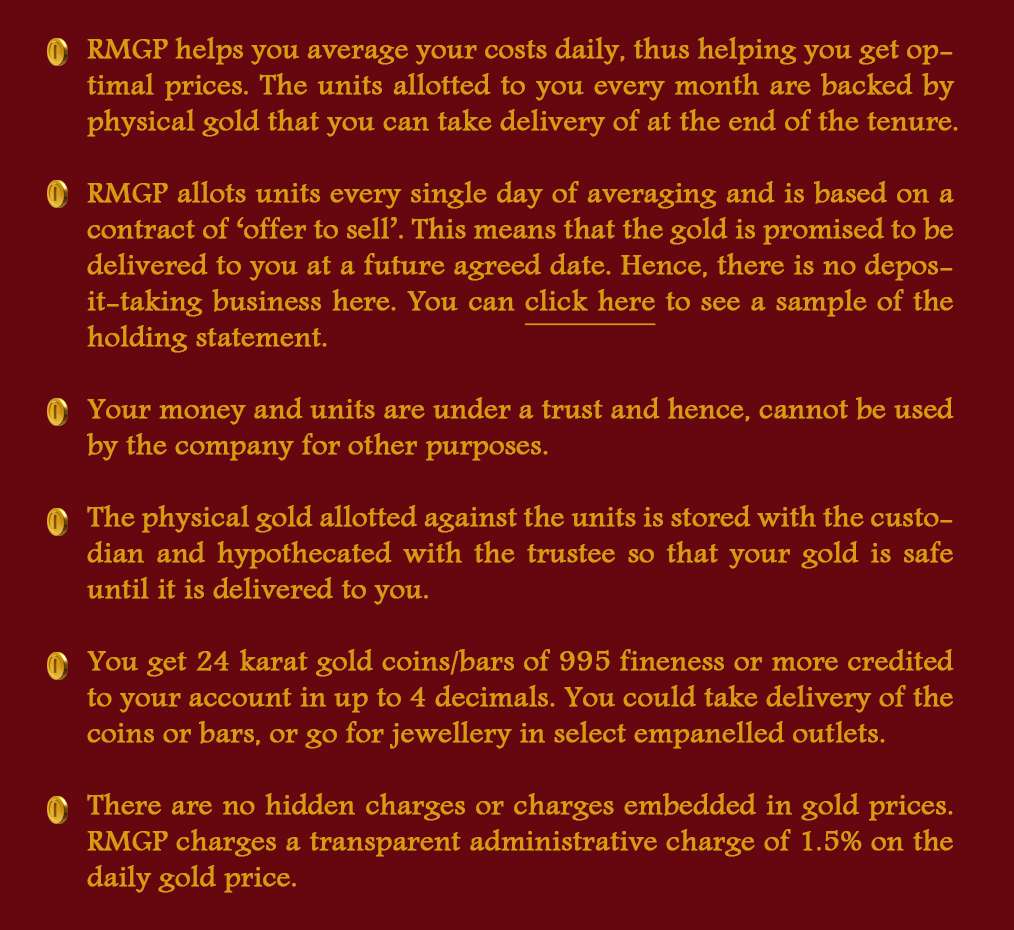

The Way Out – RMGP

If you are keen on buying physical gold, then Reliance My Gold Plan helps you overcome all the above limitations.

Besides this, you have a host of other features that make RMGP superior to jewellery schemes.

Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan

2.Reliance Tax Saver (ELSS) Fund

3.HDFC TaxSaver

4.DSP BlackRock Tax Saver Fund

5.Religare Tax Plan

6.Franklin India TaxShield

7.Canara Robeco Equity Tax Saver

8.IDFC Tax Advantage (ELSS) Fund

9.Axis Tax Saver Fund

10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online -

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

---------------------------------------------

Invest Mutual Funds Online

Download Mutual Fund Application Forms from all AMCs

0 comments:

Post a Comment